Druckenmiller: A Decade Of No Returns

By Lance Roberts | October 25, 2022

Share ![]()

Is a “lost decade” ahead for markets? Stanly Druckenmiller believes that could be the case.

“There’s a high probability in my mind that the market, at best, is going to be kind of flat for 10 years, sort of like this ’66 to ’82 time period.”

Druckenmiller added that with inflation raging, central banks raising rates, deglobalization taking hold, and the war in Ukraine dragging on, he believes the odds of a global recession are now the highest in decades. He pointed out that globalization has a “deflationary” effect because it increases worker productivity and speeds up technological advancement. However, that tailwind is now fading. To wit:

“When I look back at the bull market that we’ve had in financial assets really starting in 1982. All the factors that created that boom not only have stopped, they’ve reversed.”

But Druckenmiller isn’t alone in his views. Gerard Minack also suggests the idea of a “beta drought.” Like Druckenmiller, Minack believes the U.S. is entering a long period of low to negative asset returns for an extended period.

“Prior droughts have been due to rising inflation and/or high market valuation. The US is now at risk from both.

US investors have enjoyed munificent beta for a dozen years: a 60:40 equity/bond portfolio generated a 10½% annual average return between March 2009 and January 2022. But there have been four beta droughts since 1900: extended periods of little or no beta return. Three of the four historical beta droughts – in the 1910s, 1940s and 1970s – were caused by rising inflation, typically decade-average CPI inflation of over 5%. Those three inflation episodes were associated with WW1, WW2, and the 1970s oil shocks. The 2010s beta drought was due to excess equity valuation (like we have seen recently.) The US may now be entering another beta drought. US returns are at now risk from both the prospect of higher inflation, AND the headwind to returns from high starting-point valuations.”

Are Druckenmiller and Minack correct? Should investors be expecting another lost decade?

The Value Of Valuations

There is much to both Druckenmiller’s and Minack’s views. Over the last 120 years, valuations have consistently proved to be a strong predictor of future returns, with lost decades common. However, as we discussed previously in “Rationalizing High Valuations:”

“The mistake investors repeatedly make is dismissing the data in the short-term because there is no immediate impact on price returns. Valuations by their very nature are HORRIBLE predictors of 12-month returns. Investors avoid any investment strategy which has such a focus. In the longer term, however, valuations are strong predictors of expected returns.”

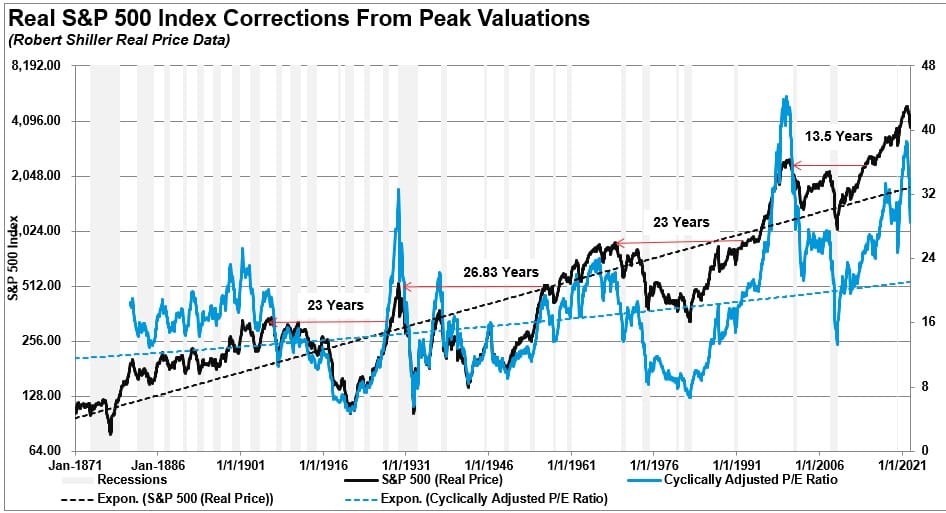

The chart below shows valuations and rolling 10-year total real returns. The obvious conclusion is that overpaying for value leads to lost decades.